How commercial storm damage is fundamentally different from residential

Commercial storm damage looks similar on the surface — wind, hail, water intrusion. But everything else about it is different. The roofing systems are different, the insurance is more complex, the stakes are higher, and the traps are worse.

Pitched roofs, shingles, homeowner policy

- Damage visible from ground — missing shingles, granules in gutters

- Water intrusion appears near breach point within hours

- Homeowner policy — relatively standardized

- No coinsurance clause in most homeowner policies

- Business interruption not relevant

- One claim covers all damage

Flat roofs, membranes, complex policy

- Flat roof damage often invisible for weeks — water travels laterally

- Leak appears 10–20 feet from actual breach — wrong repairs get made

- Coinsurance clauses penalize underinsurance severely

- Business interruption is a separate coverage — often not carried

- Multiple coverage types needed: property, contents, BI, flood

- Larger claims get more aggressive adjuster scrutiny

Why commercial roof damage is invisible — and how it finds you weeks later

The single most dangerous thing about commercial roof storm damage is that most of it isn't visible. Residential pitched roofs drain immediately — water moves to the eave and out. Flat and low-slope commercial roofs have essentially no drainage gradient. When a storm creates a membrane breach, water enters and travels laterally through the insulation layer — sometimes 10, 15, or 20 feet — before it finds a path through the deck and appears as an interior stain or drip.

This "travel effect" means the ceiling stain you're seeing in your northwest corner office may be caused by a membrane puncture on the east side of the roof. A contractor who patches only where the stain appears will miss the source. The leak returns. You file another claim. The insurer begins questioning whether damage is ongoing maintenance failure rather than storm-caused.

Visual inspection alone misses most flat roof storm damage

A competent commercial roof inspector uses infrared thermography or electronic leak detection — not just a visual walk. These tools find trapped moisture and insulation saturation that is completely invisible to the eye. If you're filing a commercial roof claim and your inspector only did a visual inspection, the damage scope is almost certainly understated. Demand a moisture scan as part of any post-storm commercial assessment.

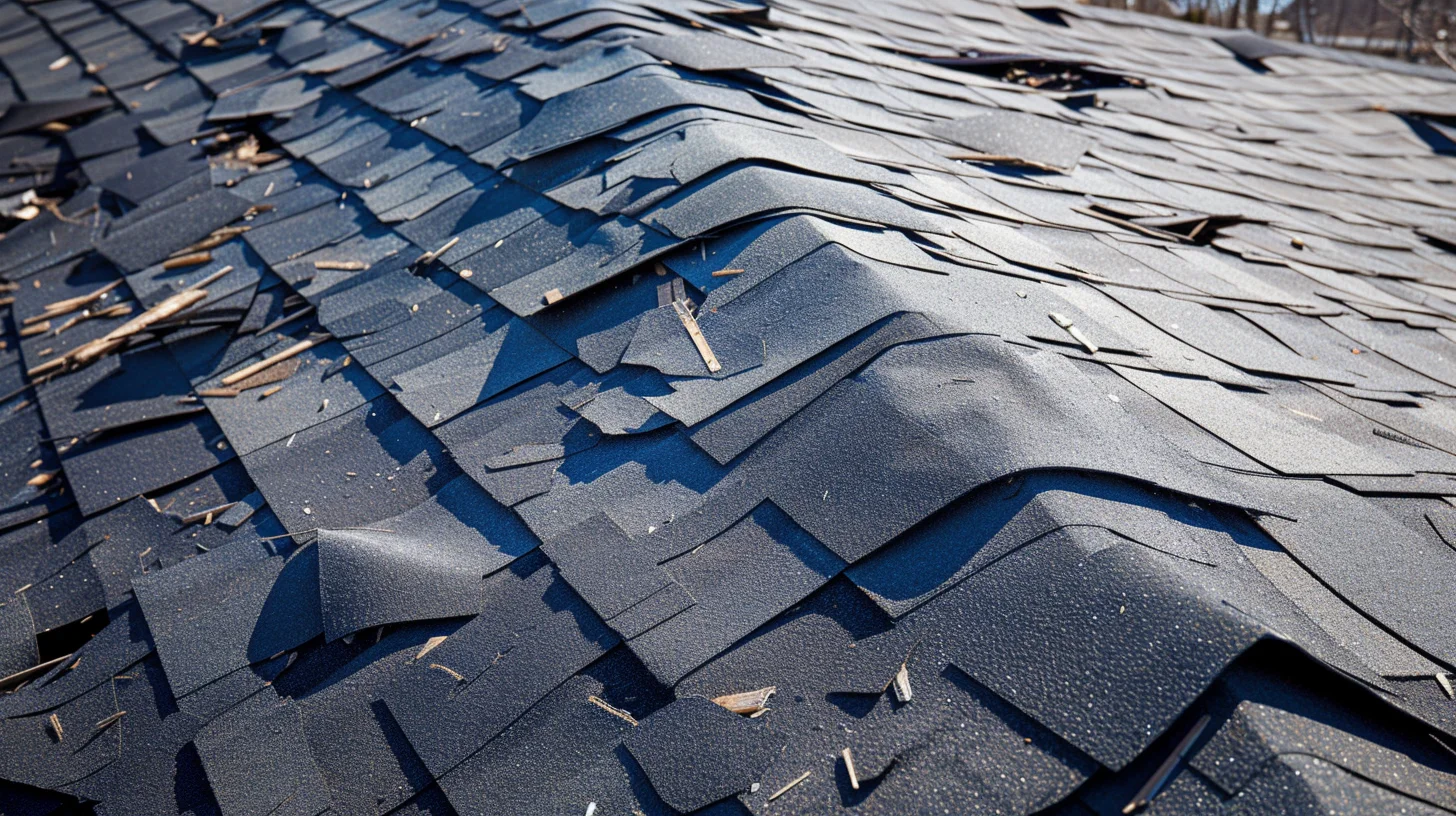

Commercial roofing systems and how storm damage presents differently on each

Most common commercial membrane

Hail creates small punctures often under one inch that are nearly invisible from ground level. Wind uplift attacks seams and edges first. Heat-welded seams can separate under hurricane-force winds. Inspect every seam and all penetration flashings with an experienced commercial roofer — not a residential contractor.

Common on older commercial buildings

More puncture-resistant than TPO but vulnerable to seam adhesive failure in extreme heat events following storms. Hail impact may not puncture immediately but creates micro-fractures that fail weeks later under UV exposure. Rubber shrinks over time — storm stress can accelerate seam separation at corners and penetrations.

Multiple-ply traditional systems

Granule loss from hail impact is visible but the real damage is to the cap sheet below. Multiple-ply systems can sustain significant underlying damage with minimal surface evidence. Blistering, delamination, and granule displacement all indicate storm impact. BUR systems on older buildings may predate current wind-uplift standards.

Standing seam and exposed fastener

Hail creates visible denting on metal panels — but the real damage is to fasteners, seams, and ridge caps. Standing seam roofs are significantly more wind-resistant than exposed-fastener systems. Inspect all fastener points, panel seams, ridge caps, and HVAC unit curbs, which are common failure points under hurricane winds.

Coinsurance — the clause that can slash your commercial claim payout

This is the most important section on this page for commercial property owners. Most homeowner policies don't have a coinsurance clause. Nearly all commercial property policies do — and most property owners don't fully understand what it means until they file a large claim and the check comes back dramatically smaller than expected.

How the coinsurance clause works

A coinsurance clause requires you to insure your commercial property for at least a specified percentage of its full replacement cost value — typically 80%, 90%, or 100%. The purpose is to prevent owners from deliberately underinsuring to save on premiums while still expecting full claims coverage.

If your building's replacement cost is $1,000,000 and your policy has a 90% coinsurance requirement, you must carry at least $900,000 of coverage. If you only carry $700,000, you are underinsured — and the coinsurance penalty applies to every claim you file, not just total losses.

That $44,444 gap exists because you were underinsured — not because of anything the storm did. The insurer pays you based on what you should have been carrying, not what you were actually claiming. This is why commercial property owners must have their building appraised for replacement cost value regularly — not just at purchase — and must update coverage limits to match.

Get a replacement cost appraisal on every commercial property you own

Construction costs on the Gulf and Atlantic coasts have increased 25–40% since 2020. A commercial building insured for its 2019 replacement cost value is almost certainly underinsured in 2026 — and subject to a significant coinsurance penalty on any claim. Have your property appraised for current replacement cost, compare it to your policy limits, and update coverage before hurricane season. Your commercial insurance broker can coordinate this review.

Business interruption — the separate claim most owners don't know to file

When a storm damages your commercial roof and forces a partial or full closure, you face two distinct financial losses: the cost to repair or replace the roof (property damage), and the revenue you lose while you're closed or operating at reduced capacity (business interruption). These are completely separate coverages that must be filed separately.

What business interruption coverage actually covers

- Lost revenue — net income you would have earned during the closure period

- Continuing fixed expenses — payroll, lease payments, loan payments, utilities that continue during closure

- Extra expenses — costs to minimize the shutdown, such as renting temporary space or equipment

- Extended period of indemnity — some policies cover the period to rebuild revenue after reopening, not just the closure itself

What business interruption does NOT cover

- Flood damage — business interruption triggered by flood requires separate flood coverage

- Utility outages from the storm that didn't directly damage your building (unless you have utility services interruption coverage)

- Losses beyond the stated indemnity period — typically 12 months, sometimes 24

- Closures caused by perils excluded from your base commercial property policy

Without business interruption coverage, a storm closure can be fatal to a business

Industry data consistently shows that roughly two-thirds of businesses without adequate business interruption coverage never fully recover from a major storm closure. The property gets repaired — but weeks or months of lost revenue, combined with ongoing fixed expenses, creates a cash crisis that outlasts the physical damage. If you own or operate a business and don't have business interruption coverage, talk to your commercial broker today. The premium is modest relative to the exposure.

How to document a business interruption claim

Business interruption claims require financial documentation that property claims don't. Your insurer will want to see:

- Prior years' revenue records — typically 2–3 years of financial statements

- Documentation of the physical damage that caused the closure (roof inspection report)

- Daily operations records showing actual closure dates and capacity reductions

- Payroll records for staff kept on during closure

- All fixed expense invoices paid during the closure period

- Records of any extra expenses incurred to minimize the shutdown

Start accumulating these records immediately after the storm — don't wait until the property claim is settled to think about the BI claim. They should be filed together or in close sequence.

The commercial storm claim process — step by step

Conduct emergency mitigation immediately

Commercial policies — like residential — require you to take reasonable steps to prevent further damage. Emergency tarping of a breached membrane, boarding of damaged openings, and deployment of desiccants or dehumidifiers in water-infiltrated spaces are all appropriate. Keep every receipt — mitigation expenses are typically reimbursable. Document everything before mitigation begins.

Get a commercial roofing specialist — not a residential contractor

This is the most critical distinction. Commercial roof systems require inspectors who understand membrane roofing, moisture mapping, and thermal imaging. A residential shingle contractor does not have the expertise to properly assess TPO, EPDM, or modified bitumen storm damage. The wrong inspection scope leads to missed damage, underpayment, and repeated leaks. Specifically request a contractor with commercial flat roof experience and moisture scanning capability.

Notify your insurer and request a commercial specialist adjuster

Large commercial claims are sometimes initially assigned to general adjusters who handle primarily residential claims. Request specifically that a commercial property specialist be assigned. Commercial roof systems, coinsurance calculations, and business interruption claims require adjuster expertise that general adjusters may not have.

Review your policy for coinsurance before the adjuster visits

Pull your commercial property policy and locate the coinsurance clause — it's usually in the Conditions section. Identify the coinsurance percentage and compare your current coverage limit to a current replacement cost estimate. If you're underinsured, know the penalty calculation before the adjuster arrives so you understand what to expect from the settlement.

File property damage and business interruption claims simultaneously

Don't wait for the property claim to be resolved before opening the business interruption claim. File both immediately. The BI claim's indemnity period typically starts on the date of loss — every day of delay in filing is a day of potential coverage that may be questioned.

Consider a public adjuster for large commercial claims

For commercial claims above $100,000, a licensed public adjuster who specializes in commercial property is almost always worth the engagement. Commercial policies are significantly more complex than residential, the coinsurance calculation creates leverage for disputes, and BI claims require financial expertise that most property owners don't bring to the table. A commercial PA's fee (typically 10–15% of additional recovery) is consistently justified on large claims.

The commercial coverage gaps that destroy businesses after storms

No flood coverage

Standard commercial property insurance does not cover flood damage — including storm surge. This is identical to residential, but the gap is often larger because commercial buildings near the coast frequently have more to lose. Commercial flood coverage through the NFIP's Commercial Flood Insurance program or private carriers is separate from property insurance and must be specifically purchased. In coastal Florida, Texas, and Louisiana, this is not optional for any ground-floor commercial tenant or building owner.

Equipment breakdown after power surges

Storm-related power surges can destroy HVAC systems, refrigeration units, servers, and production equipment. Standard commercial property policies typically exclude electrical breakdown as a covered peril — it falls under equipment breakdown coverage (also called boiler and machinery coverage), which is a separate endorsement. If you have significant equipment exposure, verify this coverage specifically.

Tenant vs. building owner — who files what

This creates significant confusion after commercial storms. The building owner's commercial property policy covers the structure. A tenant's business personal property policy covers their contents and equipment. Business interruption coverage is separate for both. After a storm, the building owner files for structural damage, the tenant files for contents and their own business interruption loss — and the two claims must be coordinated. If you are a tenant, don't assume the building owner's insurer will cover your losses — they won't.

Annual commercial insurance review — the four things to verify every May

Before hurricane season: (1) Get a current replacement cost appraisal and confirm your coverage equals or exceeds the coinsurance requirement. (2) Verify business interruption coverage is in force and the indemnity period is adequate. (3) Confirm flood coverage is in place separately. (4) Review equipment breakdown coverage if you have significant equipment exposure. Your commercial broker should be initiating this review annually — if they aren't, ask for it.